what is a deferred tax provision

It creates an opportunity for a company to carry forward it to the next year to be adjusted with subsequent profits thus reducing that years tax liability. Putting through a deferred tax charge is a way of evening out these differences so that the company doesnt overestimate its profit.

2022 Cfa Level I Exam Cfa Study Preparation

Deferred tax is the tax effect that occurs due to the temporary differences either taxable temporary difference or deductible temporary difference.

. It is the opposite of a deferred tax liability which represents income taxes owed. Deferred income tax expense is the opposite of deferred tax assets. Temporary differences Definition of temporary differences.

Around the world governments are stepping in to try and limit the impact of the pandemic by providing financial support in numerous ways from direct cash payments through to the deferral of tax payments. Learn more about Deferred Tax forms Deferred Tax Asset Deferred Tax Liability DTA and DTL Calculation etc. A deferred income tax liability results from a difference in income recognition between tax laws and the companys accounting methods per GAAP.

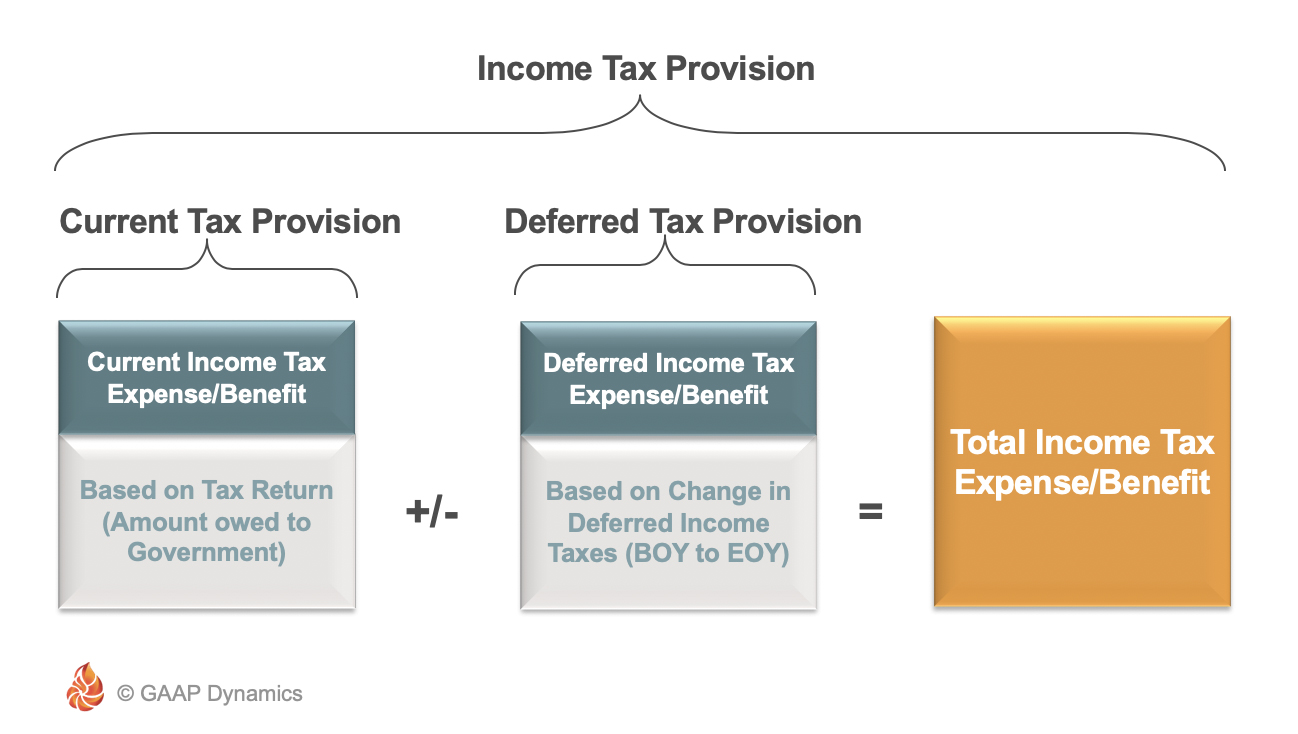

What is deferred income tax provision. Deferred income tax and current income tax comprise total tax expense in the income statement. Tax authorities charge taxes based on tax laws and the two often differ.

Deferred tax is the amount of tax payable or recoverable in future reporting periods as a result of transactions or events recognised in current or previous periods accounts. A deferred income tax is a liability recorded on a balance sheet resulting from a difference in income recognition between tax laws and the companys accounting methods. The term deferred tax refers to a tax which shall either be paid in future or has already been settled in advance.

It was written into law in March 2021 under the American Rescue Plan Act and applies to wages paid between March 27 2020 and December 31 2021. Generally FRS 102 adopts a timing difference approach ie deferred tax is recognised when items of income and expenditure are. Companies calculate book profits using a particular accounting method.

The effect arises when taxes are either not paid or overpaid. An amount drawn out from a. Deferred income tax is recognised under IAS 12 to account for differences between tax base of an asset or a liability and its carrying amount.

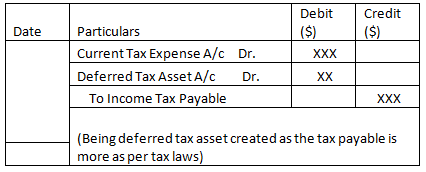

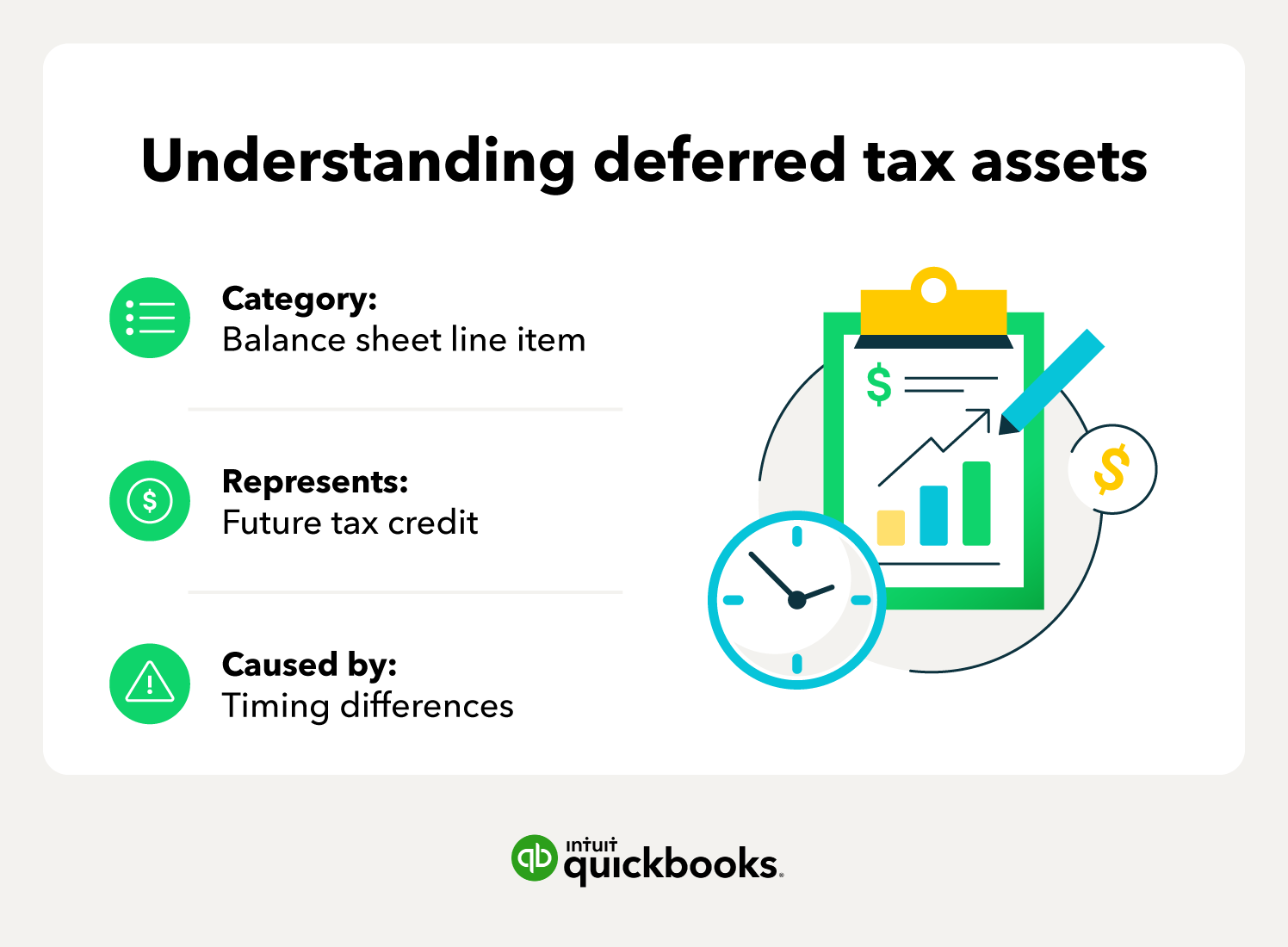

Deferred income taxes are taxes that a company will eventually pay on its taxable income but which are not yet. Deferred tax asset or DTA is recorded in the year when such loss is realised. A provision is created when deferred tax is charged to the profit and loss account and this provision is reduced as the timing difference reduces.

A deferred tax asset is an item on the balance sheet that results from overpayment or advance payment of taxes. Deferred income tax expense. Now let us see that what are the causes of its decrease.

This more complicated part of the income tax provision calculates a cumulative total of the temporary differences and applies the appropriate tax rate to that total. In this article we will see why a company may differ its tax to a subsequent fiscal year or why a company may choose to pay the tax in advance. A deferred tax asset is an asset to the Company that usually arises when the Company has overpaid taxes or paid advance tax.

The deferred income tax is a liability that the company has on its balance sheet but that is not due for payment yet. A deferred tax often represents the mathematical difference between the book carrying value ie an amount recorded in the accounting balance sheet for an asset or liability and a corresponding tax basis determined under the tax laws of that jurisdiction in the asset or liability multiplied by the applicable jurisdictions statutory. To delay payment of the employer portion of Social Security tax until December 2022.

Deferred Tax is a type of tax that levied on companies provision for future taxation as per Income Tax Act. A tax provision is the income tax corporate entities will incur based upon the companys net income for the year. Provision made for Deferred Tax etc.

The deferred income tax expense refers to a cost thats noted as a liability on your balance sheet but doesnt have to be paid just yet. This article Deferred tax provisions 123 kb sets out four key areas of your tax provision that could be affected by the impacts of COVID-19. When the amount is less than the estimated tax an entry is placed on.

For this reason the. Deferred tax asset is created when a company realises gross loss in a particular year. The payroll tax deferral provision allows small business owners in the US.

Deferred tax DT refers to the difference between tax amount arrived at from the book profits recorded by a company and the taxable income. IAS 12 defines a deferred tax liability as being the amount of income tax payable in future periods in respect of taxable temporary differences. Its also a result of the differences in income recognition between income tax accounting rules and your companys accounting.

Such taxes are recorded as an asset on the balance sheet and are eventually paid back to the Company or deducted from future taxes. A deferred tax liability occurs when a business has a certain amount of income for an accounting period and that amount is different from the taxable amount on their tax return. Difference between deferred tax asset and deferred tax liability is the difference in income that is computed as per the provisions of different laws.

A Deferred Tax Asset is an accounting term on a firms balance sheet that is used to illustrate when a firm has overpaid on taxes and is due some form of tax relief. However to understand this definition more fully it is necessary to explain the term taxable temporary differences. Deferred tax could be deferred tax asset or deferred tax liability in which it will be deductible or taxable in the future.

So in simple terms deferred tax is tax that is payable in the future. These are created because of the timing difference between the book and taxable profits. What is the payroll tax deferral provision.

A deferred tax liability is a line item on a balance sheet that indicates that taxes in a certain amount have not been paid but are due in the future.

/dotdash_Final_Deferred_Tax_Asset_Definition_Aug_2020-01-dab264b336b94f939b132c55c018f125.jpg)

Deferred Tax Asset Definition

Net Operating Losses Deferred Tax Assets Tutorial

Define Deferred Tax Liability Or Asset Accounting Clarified

:max_bytes(150000):strip_icc()/dotdash_Final_Deferred_Tax_Asset_Definition_Aug_2020-01-dab264b336b94f939b132c55c018f125.jpg)

Deferred Tax Asset Definition

Deferred Taxes Modeling Accounting Concept

Deferred Tax Liabilities Meaning Example How To Calculate

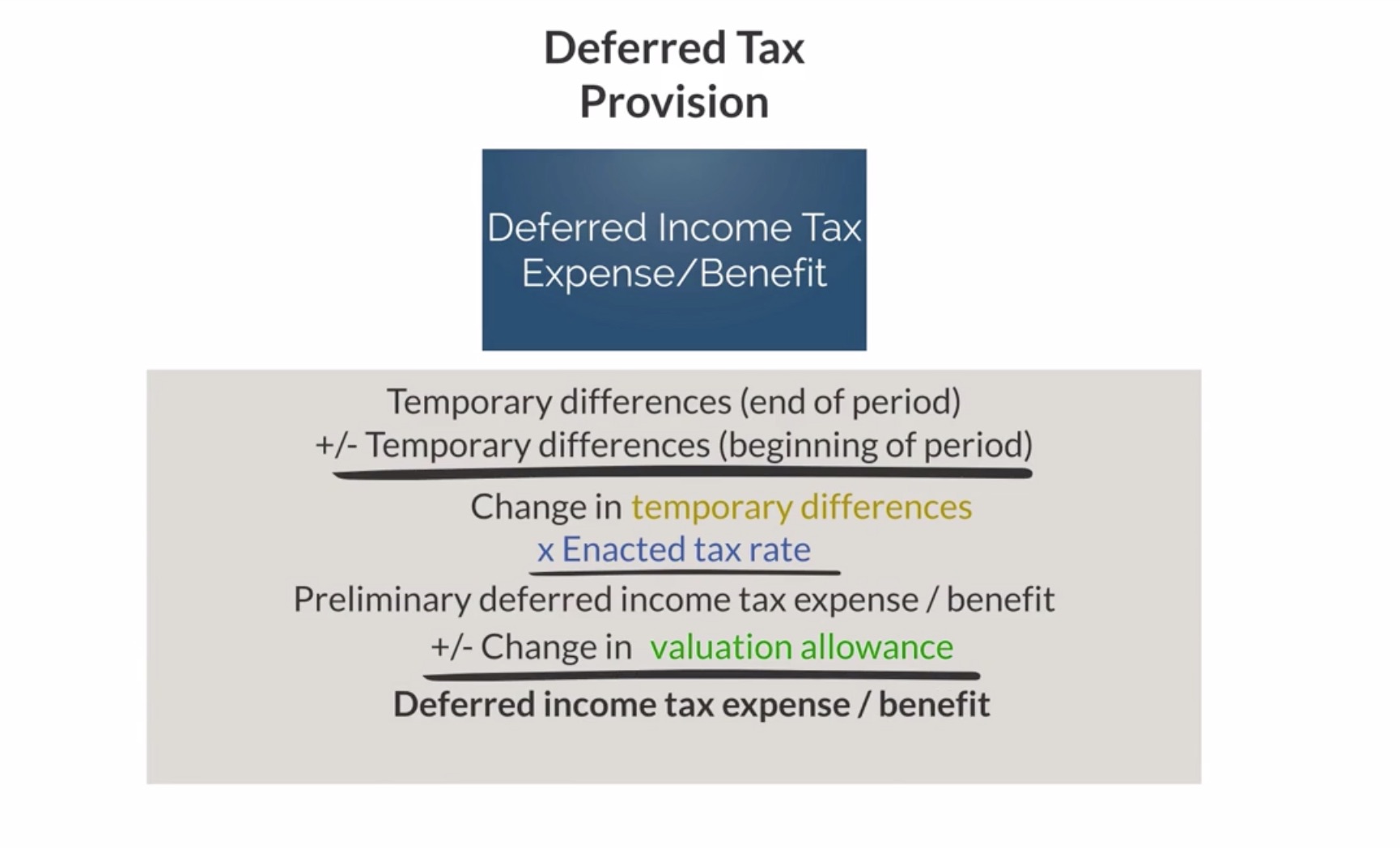

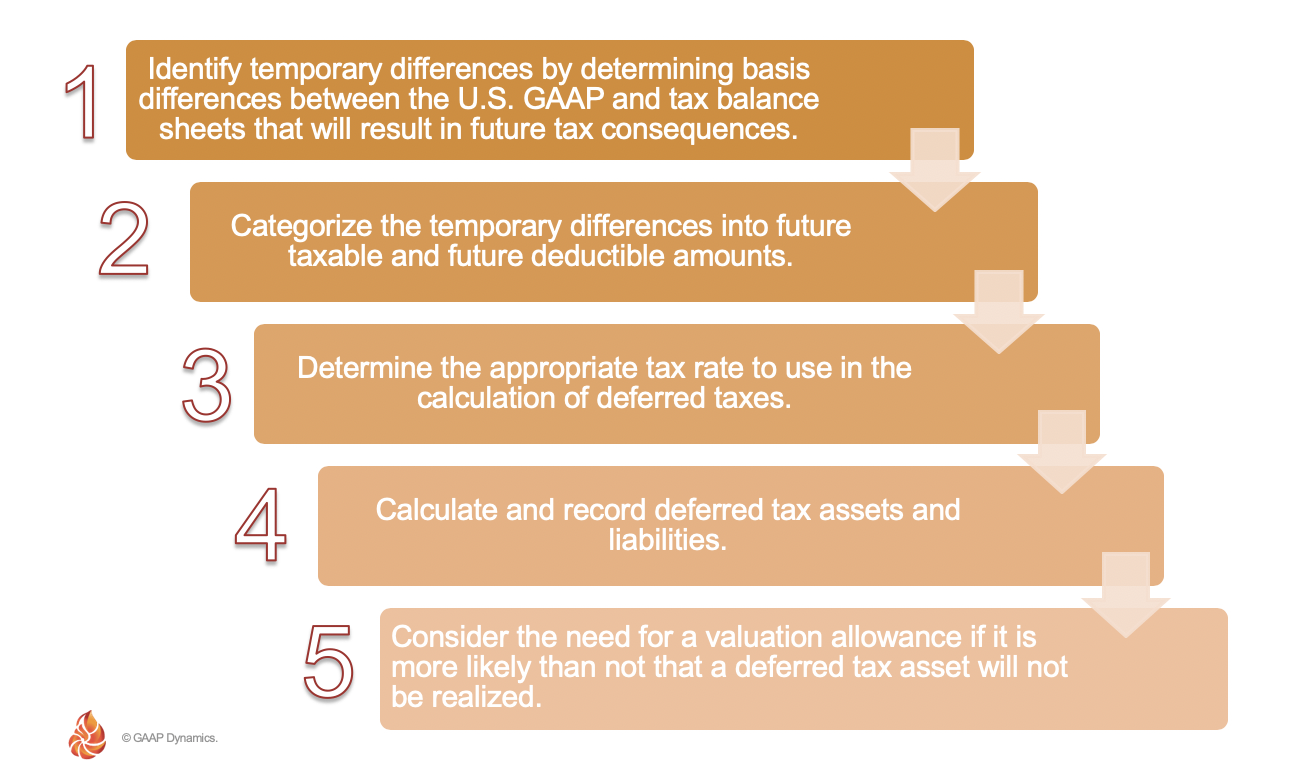

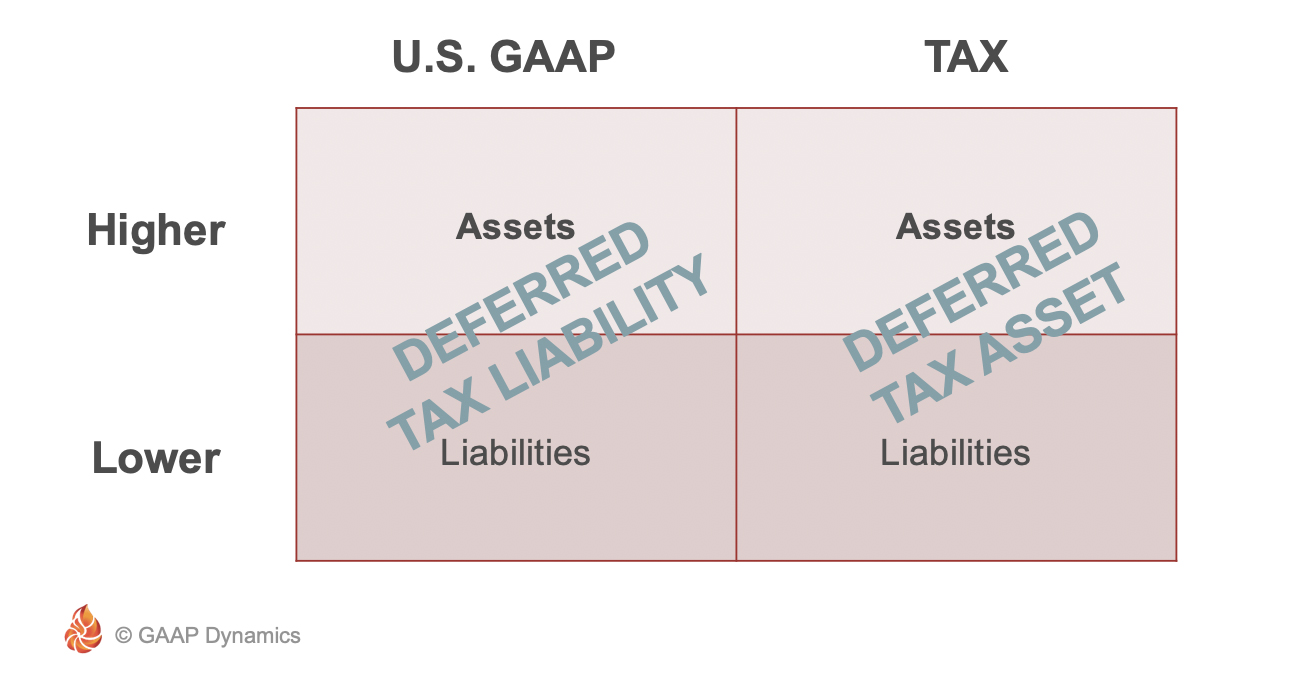

Accounting For Income Taxes Under Asc 740 Deferred Taxes Gaap Dynamics

/dotdash_Final_Deferred_Tax_Asset_Definition_Aug_2020-01-dab264b336b94f939b132c55c018f125.jpg)

Deferred Tax Asset Definition

How To Make Sure That The Deferred Tax Is An Asset Or A Liability Quora

Worked Example Accounting For Deferred Tax Assets The Footnotes Analyst

What Is A Deferred Tax Liability Dtl Definition Meaning Example

Deferred Tax Asset Deferred Tax Assets Vs Deferred Tax Liability

Accounting For Income Taxes Under Asc 740 An Overview Gaap Dynamics

What Are Deferred Tax Assets And Deferred Tax Liabilities Article

Accounting For Income Taxes Under Asc 740 Deferred Taxes Gaap Dynamics

Deferred Tax Liabilities Meaning Example How To Calculate

Deferred Tax Double Entry Bookkeeping

Accounting For Income Taxes Under Asc 740 Deferred Taxes Gaap Dynamics

Deferred Tax Liabilities India Dictionary